Return Trends At Hong Kong and China Gas (HKG:3) Aren’t Appealing

If you’re looking for a multi-bagger, there’s a few things to keep an eye out for. Firstly, we’d want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. This shows us that it’s a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. However, after investigating Hong Kong and China Gas (HKG:3), we don’t think it’s current trends fit the mold of a multi-bagger.

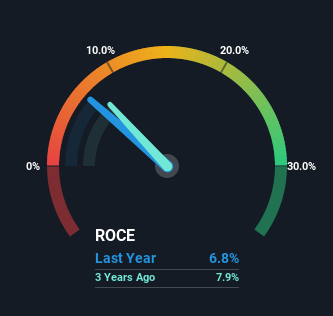

What Is Return On Capital Employed (ROCE)?

If you haven’t worked with ROCE before, it measures the ‘return’ (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Hong Kong and China Gas:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets – Current Liabilities)

0.068 = HK$8.8b ÷ (HK$168b – HK$39b) (Based on the trailing twelve months to December 2021).

Thus, Hong Kong and China Gas has an ROCE of 6.8%. Ultimately, that’s a low return and it under-performs the Gas Utilities industry average of 9.8%.

See our latest analysis for Hong Kong and China Gas

Above you can see how the current ROCE for Hong Kong and China Gas compares to its prior returns on capital, but there’s only so much you can tell from the past. If you’d like to see what analysts are forecasting going forward, you should check out our free report for Hong Kong and China Gas.

How Are Returns Trending?

There are better returns on capital out there than what we’re seeing at Hong Kong and China Gas. The company has employed 33% more capital in the last five years, and the returns on that capital have remained stable at 6.8%. This poor ROCE doesn’t inspire confidence right now, and with the increase in capital employed, it’s evident that the business isn’t deploying the funds into high return investments.

The Key Takeaway

In conclusion, Hong Kong and China Gas has been investing more capital into the business, but returns on that capital haven’t increased. And in the last five years, the stock has given away 16% so the market doesn’t look too hopeful on these trends strengthening any time soon. In any case, the stock doesn’t have these traits of a multi-bagger discussed above, so if that’s what you’re looking for, we think you’d have more luck elsewhere.

One final note, you should learn about the 3 warning signs we’ve spotted with Hong Kong and China Gas (including 2 which make us uncomfortable) .

While Hong Kong and China Gas isn’t earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does…

Read More: Return Trends At Hong Kong and China Gas (HKG:3) Aren’t Appealing